Nobody enjoys talking about insurance until they desperately need it. Then it becomes the most important conversation in the room. That gap between frustration and necessity is where property owners lose serious money.

I recently sat down with Kevin King, Senior Manager and Insurance Broker at The Gray Group Insurance Brokerage, to pull back the curtain on what is actually happening in the North Texas insurance market.

Here’s a snippet of our conversation:

Kevin is not your typical agent. He is a corporate strategist-turned-independent consultant who helped scale a small startup into a powerhouse multi-state operation. If you own a home or investment property in North Texas, you need to hear what he has to say.

Watch the full episode:

Why Independent Advocacy Trumps Corporate Convenience

The market has felt like a black box lately. Climbing premiums and shrinking options leave homeowners frustrated. To understand why, we have to look at the mechanics behind the scenes.

Kevin’s journey into this world started uniquely. After a corporate stint with Bridgestone Americas, where he ran a Firestone store, he realized that running a small business taught him more than any boardroom ever could.

“It was like running a little business. Even though it was a massive corporate entity, when you’re running a store for three years or so, you gotta manage a team of 20 different areas of expertise and age. And then the customer experience is a big part of retail. But there are all sorts of things. And then I’m doing P&Ls, we’re doing all sorts of procurement and figuring out what to stock, what not to. I mean, it’s just like running a retail business. It was an automotive shop. And I loved being able to work on cars and whatnot and all that and that experience.”

That operational efficiency mindset is exactly what he brought to The Gray Group. He joined his brother-in-law, Dylan Gray, who had started by purchasing a foundational book of business in Haskell, Texas. From there, they scaled by identifying underserved agencies and retaining rockstar local talent.

The lesson for real estate investors is clear. Sustainable expansion relies on securing strong carrier contracts and over-hiring slightly during growth phases to maintain customer service. According to the Texas Department of Insurance, market volatility often stems from carrier loss ratios. You can review the latest Texas insurance market volatility data from the Insurance Information Institute to see the raw numbers behind the premium hikes.

When you understand the commercial general liability landscape for your business properties, you start to see why independent advocacy matters. The same logic applies to your personal residence.

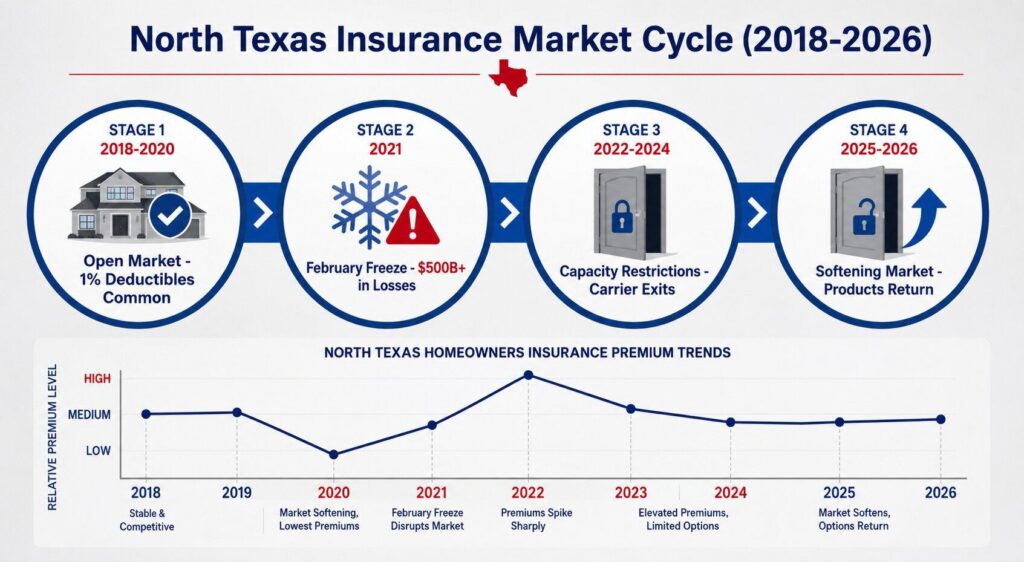

The North Texas Insurance Roller Coaster

We dug deep into why Texas premiums have felt like a roller coaster since 2018. Kevin traced the timeline from a highly competitive, open market to the catastrophic financial aftermath of the February 2021 winter freeze. That single event caused over half a trillion dollars in damages across the state.

Combine that with pandemic-era population influxes into hail-heavy zones north of Highway 121, like Prosper and Aubrey. This recent North Texas volatility analysis shows how local market swings affect everything from home values to risk assessment. Carriers faced a perfect storm of unprecedented losses and skyrocketing material replacement costs. You cannot understand your current North Texas homeowners insurance quote without knowing that history.

Here is the good news. The market is finally softening. Carriers that completely withdrew from Texas are returning to the table.

Deconstructing the Buzzwords: Deductibles and Market Value

One of the biggest pain points we addressed is the industry shift toward a standard 2% wind and hail deductible. Kevin warned that while some owners are still grandfathered into a 1% deductible, those days are rapidly ending.

We also tackled the friction between ethical adjusters and predatory roofing companies. He shared a quick story about a retired couple panicked over a $70,000 roof quote from an out-of-town solicitor. After a local inspection, they needed six shingles. A $400 bill.

“We don’t even talk to each other. I don’t even look at market value. I don’t care about market value. I care about the reconstruction costs. So I’ll structure all that, see what we can do, and guide them as best as possible. And sometimes I’ll even cut back and try something like, ‘You are way over-insured here. We don’t need to be here.’ But at the end of the day, sometimes the cheapest policy can be the most expensive policy.”

For real estate agents, this distinction is everything. A property’s market value has zero correlation with its reconstruction cost vs market value. If you look solely at a cheap premium without evaluating whether a policy is open peril or named peril, you are setting yourself up for disaster.

Understanding replacement cost valuation data from CoreLogic helps bridge this gap. When you budget for closing costs when buying a home, remember that the insurance portion should be based on rebuild cost, not sales price. The same principle applies to prepaid taxes and insurance in your monthly mortgage payment.

I always walk my clients through the first-time home buyer steps, highlighting this exact distinction. It saves them thousands.

The Silent Water Hazards Destroying Property Portfolios

Water damage claims are the most heavily litigated and misunderstood aspect of property ownership. Kevin broke down exactly how a comprehensive policy evaluates water based on the originating peril. If wind forces a door open and rain floods a room, it is wind-driven rain.

However, hidden internal leaks are where property owners lose tens of thousands of dollars. You need to verify these specific coverages in your contract.

- Sudden and Accidental Burst: Immediate events, such as a frozen pipe bursting.

- Limited Hidden Seepage (Slow Leaks): Gradual decay, like a failed shower pan rotting floors. Many carriers cap this at a restrictive $10,000.

- Water Backup: Backups from sewer lines. This requires a specific endorsement.

- Foundation Water Damage: Coverage for slab leaks or tearing out concrete to access pipes.

Recent water damage prevention research from the Insurance Institute for Business & Home Safety highlights how slow leaks cause more long-term structural damage than sudden bursts. This mirrors exactly what Kevin sees in his daily claims work.

“Your policy, I can’t tell you, I have over six figures in denied claims turning into approved claims because an adjuster maybe didn’t understand something or there was miscommunication… I’ve even had adjusters go, ‘Well, I’ve done this for 20 years.’ I’m like, ‘With all due respect, you’ve been doing this wrong for 20 years. Look how it shows it in the contract.’ I’ll pull the contract and go, ‘Actually, first of all, show me the contract where it’s denied because I know it’s approved.'”

Why Your Independent Broker Must Be a Claims Advocate

The most compelling takeaway from my session with Kevin was his stance on contract interpretation. An agent’s job does not end when a policy is bound. A truly elite broker acts as a legal advocate throughout the entire claims lifecycle.

Kevin shared a powerful example of a retired widow whose $40,000 barn was destroyed by high winds. The carrier issued a blanket denial, claiming the building needed to be explicitly scheduled. By intervening and reviewing the contract, Kevin proved the barn qualified cleanly under “other structures” coverage. He secured full funding for his client.

These are the independent insurance broker benefits that no online algorithm can replicate. When you work with someone who offers a robust Texas homeowners policy with true advocacy, you are buying peace of mind. Adding a personal umbrella insurance layer on top of that creates a comprehensive liability shield for your entire net worth.

For landlords and investors, requiring renters insurance in Texas for your tenants is a non-negotiable risk management strategy.

What Changed for Me After This Conversation

Sitting down with Kevin completely reinforced my belief that in a complex real estate market, who you partner with dictates the safety of your net worth. It is easy to jump online and buy a cut-rate policy directly from a corporate carrier. But when you do that, you lose a critical human shield.

“Building wealth is important, but protecting what you’ve built matters too. So if it’s a home or a business, having the right people in your corner does make a big difference. Find a good agent. During the claim, I’m an advocate for you. By law, I’m supposed to be an advocate for you anyway, but I want to be.”

Moving forward, I am looking at property insurance through a much more analytical lens. I am instructing my buyers to look for limited hidden water damage coverage parameters and checking water backup limits, rather than just looking at the top-line premium numbers. A real estate agent who is not pushing their clients to audit these parameters with an independent expert is leaving them exposed.

Want to hear my full conversation with Kevin King on North Texas homeowners’ insurance, the hidden water damage traps that destroy property portfolios, and why your independent broker should be a claims advocate? Listen to the complete episode of The Falls Home Front.

No Room for Extensions

I asked Brendan if extensions are ever granted due to the challenging North Texas market. His response was clear: only if the property is in a federally declared disaster area. Recent exceptions include wildfires in Hawaii and California and the COVID-19 pandemic.

The 45-day and 180-day deadlines are firm, emphasizing the need for early planning as the 45-day window arrives quickly, particularly if replacement properties aren’t identified before the sale closes.

For a current read on what North Texas inventory conditions look like heading into any exchange timeline, the latest Wichita Falls housing market update can help investors set realistic expectations for how quickly a replacement property needs to be under contract.

Listen Here

Frequently Asked Questions

Why is my North Texas homeowners insurance premium significantly higher than my direct neighbor’s?

Even if your properties feature identical floor plans, insurance underwriting relies on highly individualized actuary tables. Factors such as your personal credit-based insurance score, prior claims history, exact roofing age, and specific safety endorsements alter the baseline premium significantly. Direct comparisons are rarely accurate.

Does a standard Texas homeowners policy cover damage from rising floodwaters?

No. To my knowledge, there is not a single standard homeowners’ insurance policy in the state of Texas that provides native coverage for surface water flooding. Protecting your asset against rising river waters requires a separate policy through the National Flood Insurance Program (NFIP) or a private flood carrier. You can check the flood risk for your specific property using the FEMA Flood Map Service Center.

What is the main difference between an open peril and a named peril policy?

A named peril policy only provides financial compensation for losses caused by hazards explicitly typed out in the contract. If it is not listed, it is not covered. An open peril policy flips that framework. It covers every single source of property damage imaginable unless the specific hazard is explicitly excluded in the contract.

Connect With Kevin King

If you want to audit your current policy or just get a second opinion, reach out to Kevin directly. He actually picks up the phone.

- Phone / Text: 469-766-2999

- Email: kking@graygroupins.com

- Website: graygroupins.com

Kevin specializes in auto, home, life, and commercial insurance. He holds a business degree from the University of Arkansas and completed a leadership development program with Bridgestone Americas before joining The Gray Group in 2018. Since then, the agency has grown from a single purchased book in Haskell, Texas, to 11 offices across three states with 27 employees.

Apply as a Guest Speaker

The real estate landscape is evolving rapidly. Capital is shifting. Underwriting guidelines are tightening. Risk management is more critical than ever before. If you are actively working in the industry and solving real-world problems in construction, asset protection, commercial development, brokerage, or real estate finance, I would love to feature your expertise on our stage. Apply now through the Lockhart Real Estate Team website.

Disclaimer: This content is for informational purposes only and does not constitute legal, tax, or financial advice. Insurance coverage depends on individual policies, carriers, and circumstances. Always consult a licensed insurance professional regarding your specific situation.

About Tim Lockhart

Tim Lockhart is a Wichita Falls Sheppard AFB PCS Home Selling & Exit Strategy Specialist for military homeowners. He works with active duty personnel preparing for PCS moves to help them determine the right strategy for their home—whether to sell, hold, or adjust timing—before executing the plan. Tim is a REALTOR® with Keller Williams Wichita Falls and a RamseyTrusted real estate agent. He is a retired U.S. Air Force officer with over a decade of experience helping clients navigate complex, time-sensitive real estate decisions in Wichita Falls, Burkburnett, and Iowa Park. If you have PCS orders and need a clear plan for your home, schedule a consultation to map out your next step.- Kevin King of The Gray Group Insurance Brokerage Unpacks Property Protection, Market Shifts, and Policy Traps - June 30, 2026

- Is a VA Loan Weaker Than a Conventional Loan? What Sellers Should Know - June 27, 2026

- Why Are 1 in 6 North Texas Home Sales Falling Through, and How Do You Bulletproof Yours? - June 25, 2026

- What Does the May 2026 Housing Market Look Like in Wichita Falls? - June 24, 2026

- Should You Sell or Rent Your House When You Get PCS Orders at Sheppard AFB? - June 24, 2026

- From Hobbyist to Award-Winning Winemaker: My Conversation with James Hanger of OG Cellars - June 23, 2026

- How to Protect Your Real Estate Wealth with Brendan Lewis Asset Preservation Inc - June 23, 2026

- How Public Art Drives Real Estate Value and Community Growth: A Conversation with David Baker - June 22, 2026

- Things to Do for America’s 250th Birthday Near Wichita Falls, Texas | 4th of July 2026 Guide - June 2, 2026

- Beyond the 20% Myth: How Andrew Postell and CrossCountry Mortgage are Decoding Real Estate Wealth - June 1, 2026