You are always paying a mortgage. The only question is whether it’s yours or your landlord’s. That single idea is the foundation of every wealth-building conversation I have.

In a recent episode of The Falls Homefront, I sat down with Andrew Postell from CrossCountry Mortgage to dismantle the biggest myths holding people back. We talked about why the 20% down rule is outdated, how veterans can access rates in the 5% range, and the real truth behind the BRRRR method.

If you’re curious, here’s a snippet of our conversation:

Andrew has 25 years of experience. He crafts wealth strategies, not just loans. This discussion helps you overcome market “analysis paralysis” and understand current financing tools.

Here is why I am betting on strategic lending over market timing.

Watch the full episode:

Why I'm Betting on Strategic Lending Over Market Timing

I’ve sat in investor groups with Andrew for years. There’s a reason he is in the top 1% of loan officers nationwide. You can see his professional background on his LinkedIn profile. He doesn’t think like a banker. He thinks like an owner.

I wanted to have this conversation to cut through the “wait for lower rates” noise. Andrew brings a level of candor that’s rare in this industry. I wanted his direct take on how he is helping people navigate the current Texas landscape without a massive pile of cash.

According to data from the Texas Real Estate Research Center, the state’s population has doubled over the last 40 years, a trend no other state matches. This influx keeps demand high. Andrew noted that waiting for a market crash is a losing game.

In fact, a report from the National Association of Realtors consistently shows that homeowners build significantly more wealth than renters over a lifetime. The math does not lie.

"The best time, Tim, was five years ago. Right? Or if you want to go back 10 years, even 10 years ago was better than five. So guess what you're going to be saying in five years from now? I wish I had bought five years ago. It's only getting harder. I can't change our society. I can't change the economy by myself. But I do know that in five years, it's gonna be even harder than it is today. It's just the world that we live in. So I can either buckle down and buy a house now or wait. But when it's harder, now is the time to do it."

Before you try to time the market, take a look at whether the Wichita Falls housing market is shifting right now. Understanding local trends is half the battle.

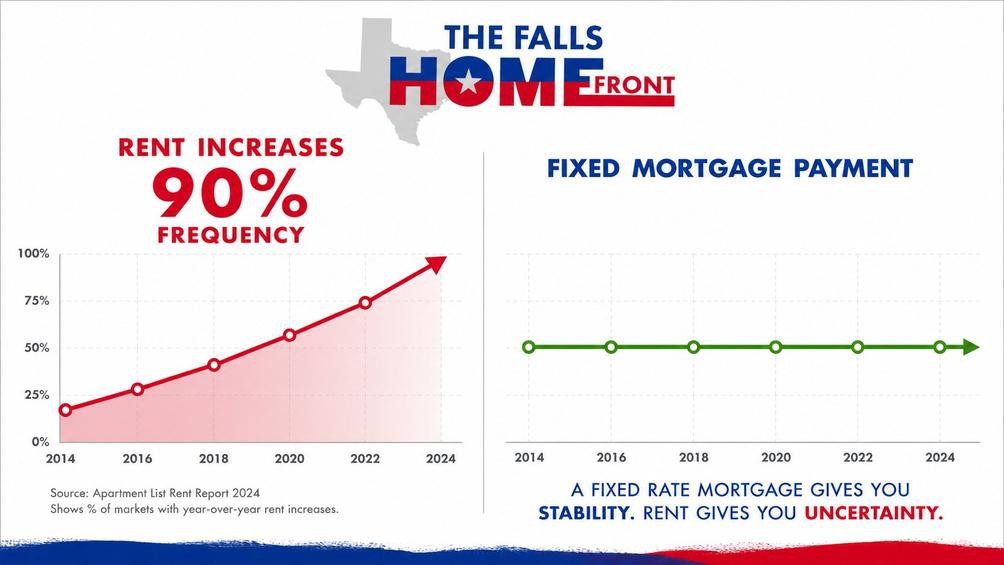

The Math Behind the "Rent Trap"

We hit on a point that most people miss. When you rent, you aren’t just “paying for a roof.” You are stabilizing someone else’s financial future.

In our market, Andrew points out that landlords increase rents roughly 90% of the time. When inflation hits, your rent goes up. When the roof needs replacing, the landlord raises the rent to cover it. As a tenant, you have zero control over your largest monthly expense.

When you own a fixed-rate mortgage, you stabilize your housing costs for 30 years. You capture the appreciation that usually goes into someone else’s pocket. Even if you move, you can keep the property and let the tenant pay down your balance. If you are curious about current rates, you can check refinance mortgage rates to see what kind of stability might be available to you.

Unlocking the Best Loan Product in Existence

As someone who used a VA loan for my first property, I was fired up to hear Andrew’s take on current military benefits. For my veteran listeners, this is your unfair advantage.

If you are waiting to save 20% down, you are working too hard. Andrew broke down how the Texas Veteran Land Board benefits are effectively giving veterans rates in the 5% range, while the rest of the world is stuck in the 6s or 7s. This is not a gimmick. It is a state-funded rate buy-down.

"The VA loan is the best mortgage out there, my man. I don't know if they give us really good health benefits, but they can put us into debt really quickly! Zero percent down, there's no PMI, and it's the lowest interest rate you can find. Even here in Texas, we have a Texas Veteran Land Board that helps buy down the rate. If you're a disabled veteran, it's an unbeatable rate—it's in the fives right now while everybody else is in the sixes. This Texas Veteran Land Board buys the rate down for you to help you get a lower rate on your mortgage."

If you are a military family looking to plant roots near Sheppard AFB, you need to look at VA home loans for Texas military families with these specific tools. Andrew Postell from CrossCountry Mortgage and his team specialize in home purchase loans that maximize these veteran benefits.

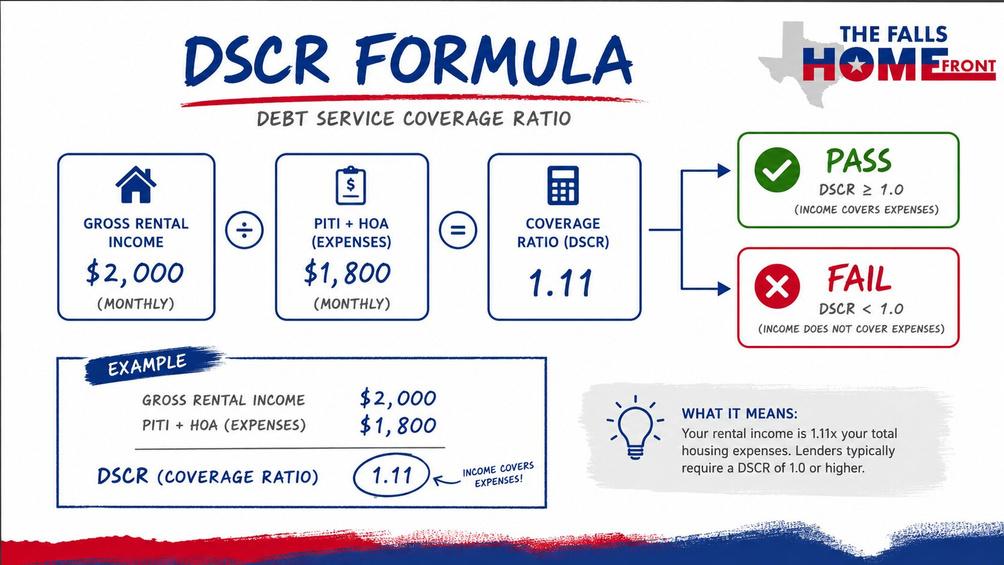

Scaling Your Portfolio Using DSCR Financing

We moved into the “pro” side of investing. If you’ve been told you hit your debt-to-income (DTI) limit, DSCR is the bridge you need.

DSCR loan requirements are different than traditional loans. Andrew explained that this loan doesn’t care about your W-2 or your tax returns. It cares about the property’s ability to pay for itself. If the rent covers the note (plus taxes and insurance), the deal moves forward. This is how you scale past the four-mortgage limit imposed by conventional banks.

For those exploring investment options, Andrew noted a crucial detail. Single-family homes might need 25% down, but multi-family properties often drop to 20% down because the cash flow is stronger.

If you already own a home, you might also look at home equity options to fund that down payment. The DSCR loan market experienced significant growth with over $2 billion in loans originated in January alone, highlighting how this product is reshaping the investment lending landscape.

The "Not-So-Easy" Truth About the BRRRR Method

I had to ask Andrew about the BRRRR method reality check. Social media makes it look like a get-rich-quick scheme. His response was the reality check we needed.

He’s been doing it since the beginning. It is a powerful way to grow with limited capital, but it is “not easy.” We discussed the high cost of hard money and the absolute necessity of having a clear exit strategy for a permanent loan.

"The BRRRR method absolutely works. I still do it to this day. It's just a lot harder than some TikTok videos or Facebook videos like to talk about. My choice was either 'impossible'—saving 25% down—or 'not easy.' I just chose the not-easy route. You can absolutely do it, but you need to make sure that you're understanding each step of the process along the way and finding a good person you can bounce ideas off of."

If you are trying to figure out your financing strategy, understanding the steps to buying your first house in Wichita Falls can help you avoid common rookie mistakes. Andrew also offers a home value estimator that is useful for calculating potential after-repair value on BRRRR deals.

Why a $5 Savings Habit is More Important Than Your Loan Rate

This was the most impactful part of our chat. It wasn’t a complex technical strategy. It was about the “muscle” of consistency.

Andrew’s challenge to save just $5 per paycheck is about building the discipline required to hold real estate long-term. Success isn’t a one-time event. It is a habit.

"All of us who have many properties and are very successful, we usually live just a little bit below our means. That way we save money to buy real estate. If you do not have a habit of saving money, I need you to start with $5 every paycheck for the next three months. I need you to create the habit. The habit is more important than the $5 every paycheck for the next three months. I need you to create the habit. The habit is more important than the $5. After you establish a habit, you'll get used to it, you'll increase it, and you'll be able to buy that house before you know it."

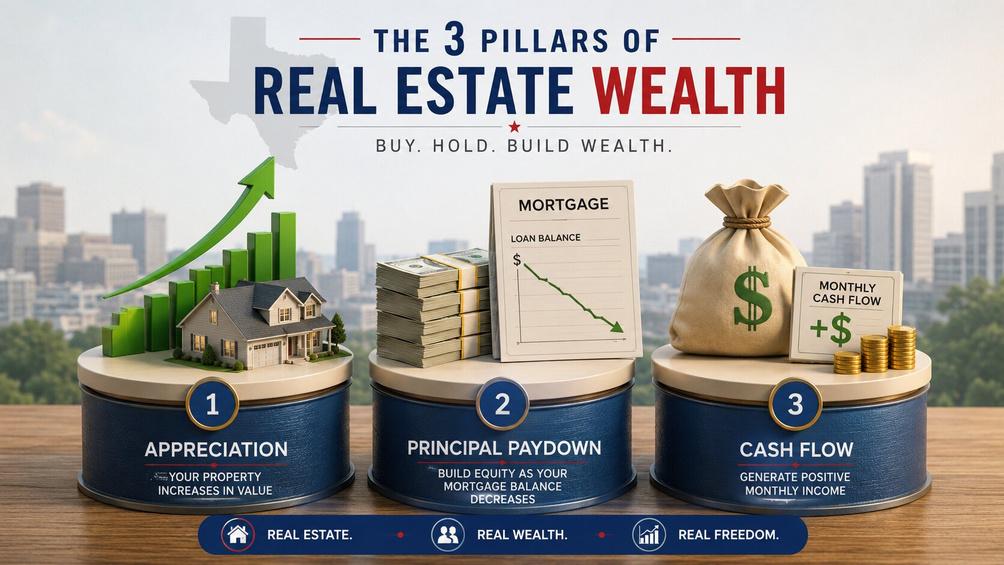

This is the core of real estate wealth building habits. It isn’t about timing the rate. It is about having the cash flow to act when the opportunity presents itself. A true buy and hold real estate strategy works because time in the market beats timing the market.

If you are a first-time buyer in Wichita Falls, this habit alone will put you ahead of 90% of other potential buyers.

Want to hear my full conversation with Andrew Postell about VA loans, DSCR financing, and the real truth about building wealth through real estate? Tune into this episode of The Falls Homefront.

Listen Here

Texas Real Estate FAQ

Is it too late to buy into the Texas market?

According to Andrew, the “best” time was years ago, but the second best time is now. With the population doubling over the last 40 years, the demand is only going to make entry harder in the future.

What is the main difference between a VA loan and a DSCR loan?

A VA loan is for your primary residence with zero down and no PMI. A DSCR loan is for investment properties where the qualification is based on the property’s income rather than your personal finances.

Can I get an investment property with 20% down?

Yes. Andrew noted that while single-family DSCR loans often require 25%, multi-family properties can often be secured with 20% down.

Stop Waiting. Start Building.

Building wealth in real estate is not about finding the secret path. It is about taking the obvious path that most people are too scared to walk.

I challenge you to do two things this week. First, stop trying to time the market. Second, start the habit. Put the $5 aside. Call a lender.

If this episode helped you, share it with a friend. Let’s help our whole community stop renting and start owning. You can contact me through my website at Tim Lockhart Homes or give me a call at 940-228-1730.

Apply as a Guest Speaker

Real estate is evolving. Capital is shifting. Markets are tightening. If you’re actively working in the industry and solving real problems, whether in construction, finance, brokerage, or development, we’d love to hear from you.

*This podcast is produced by the Icons of Real Estate – #1 Real Estate Podcast Network. For more resources on growing your show or refining your message, explore the podcast framework and read success stories from other industry professionals who have leveraged this platform, or apply to be a guest.*

About Tim Lockhart

Tim Lockhart is a Wichita Falls Sheppard AFB PCS Home Selling & Exit Strategy Specialist for military homeowners. He works with active duty personnel preparing for PCS moves to help them determine the right strategy for their home—whether to sell, hold, or adjust timing—before executing the plan. Tim is a REALTOR® with Keller Williams Wichita Falls and a RamseyTrusted real estate agent. He is a retired U.S. Air Force officer with over a decade of experience helping clients navigate complex, time-sensitive real estate decisions in Wichita Falls, Burkburnett, and Iowa Park. If you have PCS orders and need a clear plan for your home, schedule a consultation to map out your next step.- Can I Sell My Wichita Falls Home Remotely After I Leave for PCS? - August 4, 2026

- Cameron Turnquist of Arrowhead Builders Breaks Down Smart Wichita Falls Remodeling Decisions - August 3, 2026

- How Albert Slap of Risk Footprint Property Risk Assessments Uncover Hidden Home Risks - July 27, 2026

- What Should I Fix Before Listing My Home If I’m Leaving on a PCS Timeline? - July 24, 2026

- How Matt Mitchell of James Andrews Custom Homes Builds High-Performance Homes That Last for Generations - July 21, 2026

- Why Did the Wichita Falls Median Home Price Drop 10% in June 2026? - July 20, 2026

- What Are the Long-Term Wealth Benefits of Keeping Your Sheppard AFB Home as a Rental Instead of Selling? - July 17, 2026

- What Does the Skybox Data Center Mean for Wichita Falls Home Prices and Rent? - July 16, 2026

- How Jeremy Houchens of Priority Maintenance Saves North Texas Property Owners Thousands - July 16, 2026

- How Soon Should I List My Wichita Falls Home After Getting PCS Orders From Sheppard AFB? - July 10, 2026