Eddie Speed of Note School Explains Why Becoming the Bank Beats Being a Landlord Right Now

Five years ago, rental property math worked differently. Now, expenses outpace rent increases, thinning cash flow and leaving many investors quietly frustrated. That’s exactly why the Eddie Speed Note School Colonial Funding Group approach caught my attention.

Here’s a preview of this conversation:

That’s why I wanted to bring Eddie Speed onto The Falls Homefront. Eddie is the founder of Note School and Colonial Funding Group. With 46 years in note investing real estate, and over 50,000 transactions, he has trained thousands on the financial aspects of real estate.

This conversation redefines real estate wealth beyond owning rentals, highlighting the Eddie Speed Note School Colonial Funding Group’s approach.

Frankly, it changed the way I am thinking about a few things. Whether you are already active in the real estate investor network here in Wichita Falls or just getting started, this strategy deserves your attention.

Why I Had This Conversation

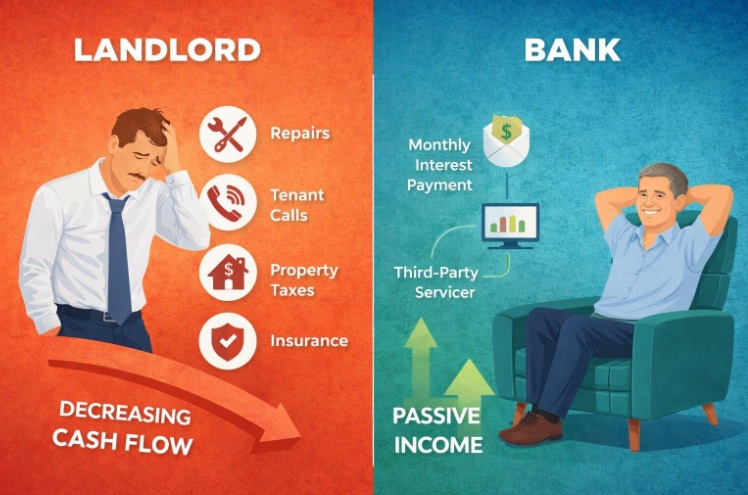

I have been watching a shift in our local market in Wichita Falls and across North Texas. The single biggest thing Eddie brought to this conversation was clarity on why so many landlords are quietly struggling right now. It is not bad luck. It is math.

Inflation led to rent increases, but expenses rose more significantly, causing a financial gap. Profitable properties now struggle to break even before mortgage payments. This situation demands strategy, as Eddie notes, it’s more profitable to be a lender than a landlord. Investors, however, remain fixated on rentals without reassessing the numbers.

"The landlord gets what's left over. The bank gets the first money out of the rent. And he has to understand that he's collecting interest — that's why people write about things like compound interest is the eighth wonder of the world. I'm telling you, interest is a real thing. Now you get paid whether you're awake or sleeping."

The actionable aspect of this situation is its cyclical nature. Eddie, who loves real estate, observes the current winning side of transactions, which is the bank side.

What It Actually Means to "Be the Bank"

The conversation turned practical: you don’t need a banking license or a finance degree to be the bank. Instead of owning property and collecting rent, you hold the mortgage note and collect interest. The Eddie Speed Note School Colonial Funding Group system breaks this down into simple, repeatable steps.

When Eddie explained, it changed my perspective. Rent is residual income after expenses, while interest is priority income—structured, predictable, and paid first monthly by a third-party servicer handling collections and reporting.

For those new to mortgage note investing beginners, this is the core concept to grasp. Unlike the appreciation game, which is essentially betting on future value you haven’t earned yet, interest is money in your pocket right now. As Eddie put it: Appreciation is money you are going to get tomorrow. Interest is money you are getting today. Eddie offers personal training for those ready to go deeper into the mechanics of real estate.

How Rental Owners Can Convert to Owner Financing

Eddie showed how rental owners can switch practically, using a real process. Note School has a system for this, and Eddie has modeled thousands of properties.

The process involves selling your rental property to a buyer using a seller financing strategy. This means you become the lender instead of cashing out and walking away. Your buyer makes monthly payments to you, secured by a first mortgage on the property. You stop being a landlord and start being the bank on that same asset.

"If a rental property is netting you about 4% a year, which is about what the norm is at the moment, a loan is going to net you about 9 or 10%. Which would you rather have, 4 or 9, or 10? Obviously. So what happens in real estate is sometimes the bank is better than the physical rental, and sometimes the rental is better than being with the bank. It's not always one."

A common concern is needing full ownership first. Eddie says you don’t; selling part of future note payments can provide liquidity to pay your mortgage while still benefiting.

The other big opportunity here is for real estate agents. Eddie made this point directly. Landlords ready to convert their rentals still need a professional to help them sell to a new buyer. Most realtors have not been trained in seller finance transactions.

But those who learn it immediately differentiate themselves in a market where total home sales have dropped. One of Eddie’s students documented the exact process in a piece called From Rental Headaches to Passive Income, which walks through a real-world conversion of owner financing rental property.

Step-by-Step: How a Rental Owner Converts to Seller Financing

- Assess Property Value: Determine the current market value of the rental.

- Find Qualified Buyer: Locate a buyer who may not qualify for traditional bank loans but has a down payment and steady income.

- Structure Note Terms: Set the interest rate, monthly payment, and loan duration.

- Close the Sale: Transfer the property deed while retaining the mortgage note.

- Collect Payments: A third-party servicer collects payments and handles IRS reporting.

Starting From Scratch

Not everyone coming to this conversation has a rental to convert. Some people are just getting started and want to know if note investing is accessible to them from the beginning. The answer, according to Eddie, is yes.

Note School has been teaching people how to be the bank real estate for 25 years. You don’t have to create a note from scratch. You can purchase notes that already exist in the market. Some of those notes are performing, meaning the borrower is paying on time. Some are non-performing, where the borrower has fallen behind. Each offers different return profiles and strategies. The Eddie Speed Note School Colonial Funding Group training covers all of these scenarios.

What Eddie consistently emphasizes is that note investing does not require you to become an expert in every detail. You need to understand how to vet the borrower’s track record, how to assess the property’s value with outside help, and how to structure your investment with appropriate leverage. The rest can be outsourced, just like the bank does.

He announced that by year-end, his team will trade loans on blockchain, allowing investors to buy fractional note interests, which offer smaller entry points, liquidity, and transparency. It’s not crypto investing; blockchain ensures verifiable transactions. His team has also published a broader overview of income-generating strategies titled 5 Smart Assets to Generate Income, which puts note investing in perspective alongside other options.

What Changed for Me After This Conversation

I started this episode aware of Eddie’s industry reputation but didn’t realize how relevant his strategy is for Wichita Falls and North Texas. Landlords here have long relied on outdated economic conditions. It’s not a failure, just a market cycle. The key is to adapt strategies to current conditions, not wait for the past to return.

"I think owning a rental house is hard. Owning a note is easy. I'm going to go have some third-party company that collects the payments and deals with interest income for the IRS, and monitors the taxes on the property and the insurance. All of that stuff that needs to happen doesn't have to be me."

That line resonated. Traditional real estate investing involves operational challenges like tenants and maintenance. Eddie’s model removes these, focusing on consistent, interest-bearing income that builds wealth passively.

If you are tired of the headaches of physical properties and want to explore owner financing rental property conversion, I highly recommend digging deeper into this strategy. Eddie set up dedicated starter training for The Falls Homefront audience at noteschool.com/falls. The Eddie Speed Note School Colonial Funding Group methodology has helped thousands of investors make this exact transition.

For those interested in note investing real estate, this is your sign to look beyond the traditional path. And if you want to learn alongside other local investors who are actively pursuing creative strategies like this, the Real Estate Investor Network and Meeting here in Wichita Falls is a great place to start those conversations.

Want to hear my entire conversation with Eddie Speed on why becoming the bank beats being a landlord right now? Listen to the full episode.

Listen Here

Frequently Asked Questions

What is a mortgage note, and how is it different from owning property?

A mortgage note is a legal document representing a borrower’s promise to repay a real estate-secured loan. As the note holder, you own the debt, not the property. The borrower pays you monthly, and the property is collateral, but the borrower handles daily responsibilities.

Do you need a lot of money to start investing in mortgage notes?

Eddie Speed teaches techniques for investors to participate in note deals without fully using their own capital. Emerging blockchain platforms will enable the purchase of fractional shares of notes, lowering investment entry points. Understanding the system is crucial before investing capital.

Is seller financing risky for the person carrying the note?

Investment risks are manageable with borrower vetting, property valuation, and professional loan documents. Note School teaches responsible underwriting, differing from property holding risks.

Can a realtor help clients convert their rental to seller financing?

This is a major opportunity for agents. Rental owners need professionals to sell properties with seller financing, attracting more buyers. Realtors who grasp this process can tap into a neglected seller segment.

Apply to Be a Guest on The Falls Home Front Podcast

Real estate is evolving. Capital is shifting. Markets are tightening. The strategies that worked five years ago are not delivering the same results today. That is exactly why I started this show.

The Falls Homefront is dedicated to spotlighting professionals who are actively solving real problems in Wichita Falls and North Texas. If you are working in brokerage, investment, finance, development, or property management, and you have a perspective that would help our community make smarter moves, I would love to have you on the show.

*This podcast is produced by the Icons of Real Estate – #1 Real Estate Podcast Network. For more resources on growing your show or refining your message, explore the podcast framework and read success stories from other industry professionals who have leveraged this platform, or apply to be a guest.*

About Tim Lockhart

Tim Lockhart is a Wichita Falls Sheppard AFB PCS Home Selling & Exit Strategy Specialist for military homeowners. He works with active duty personnel preparing for PCS moves to help them determine the right strategy for their home—whether to sell, hold, or adjust timing—before executing the plan. Tim is a REALTOR® with Keller Williams Wichita Falls and a RamseyTrusted real estate agent. He is a retired U.S. Air Force officer with over a decade of experience helping clients navigate complex, time-sensitive real estate decisions in Wichita Falls, Burkburnett, and Iowa Park. If you have PCS orders and need a clear plan for your home, schedule a consultation to map out your next step.- Can I Sell My Wichita Falls Home Remotely After I Leave for PCS? - August 4, 2026

- Cameron Turnquist of Arrowhead Builders Breaks Down Smart Wichita Falls Remodeling Decisions - August 3, 2026

- How Albert Slap of Risk Footprint Property Risk Assessments Uncover Hidden Home Risks - July 27, 2026

- What Should I Fix Before Listing My Home If I’m Leaving on a PCS Timeline? - July 24, 2026

- How Matt Mitchell of James Andrews Custom Homes Builds High-Performance Homes That Last for Generations - July 21, 2026

- Why Did the Wichita Falls Median Home Price Drop 10% in June 2026? - July 20, 2026

- What Are the Long-Term Wealth Benefits of Keeping Your Sheppard AFB Home as a Rental Instead of Selling? - July 17, 2026

- What Does the Skybox Data Center Mean for Wichita Falls Home Prices and Rent? - July 16, 2026

- How Jeremy Houchens of Priority Maintenance Saves North Texas Property Owners Thousands - July 16, 2026

- How Soon Should I List My Wichita Falls Home After Getting PCS Orders From Sheppard AFB? - July 10, 2026