Subject 2 Real Estate Investing: Strategy, Risks, and Real-World Execution

What if you could buy a house without qualifying for a mortgage, without perfect credit, and without a pile of cash?

The idea of buying a house without qualifying for a mortgage, without great credit, and without a pile of cash sounds like a scam. But there’s a strategy that makes it possible, and it’s called subject 2 real estate.

Subject 2 real estate investing is a creative financing strategy that allows you to take ownership of a property while leaving the seller’s existing low-interest mortgage in place. In today’s market, where interest rates have climbed significantly, this approach has moved from creative financing curiosity to a legitimate wealth-building strategy.

I sat down with Roger Paschal, Texas-based investor, author of Subject 2: How to Buy Property with No Credit or Money Down, and someone who has completed hundreds of these deals across more than forty states. What he shared about the strategy, the risks, and the ethical execution changed how I think about creative financing real estate.

Why Subject 2 Real Estate Is Back in Focus

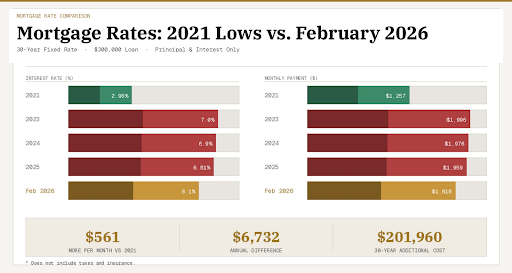

Between 2019 and 2023, millions of homeowners were locked in interest rates between three and four percent. Some secured rates are even lower. One investor Roger worked with picked up a property at 0.8 percent.

Those loans don’t exist today.

If you walk into a bank right now, you’re looking at rates in the high sixes or sevens. That difference of three to four percentage points on a mortgage payment can mean hundreds of dollars each month. For an investor focused on cash flow, that spread separates profitable deals from break-even propositions. This is the low-interest-rate mortgage takeover opportunity in action.

The numbers tell the story. On a $300,000 loan, the difference between 2021 rates and today’s rates exceeds $500 per month. That’s over $6,700 annually and more than $200,000 across a typical 30-year term.

This is why Subject 2 real estate has reemerged. The opportunity to acquire loans at historically low rates, combined with homeowners who need to move but lack equity, creates a genuine win-win. Sellers solve their problem, and investors acquire paper that actually works in their favor.

But as Roger emphasized, this is not about finding free houses or using clever tricks. This is a strategic acquisition that requires education, preparation, and ethical execution.

What Is Subject 2 Real Estate?

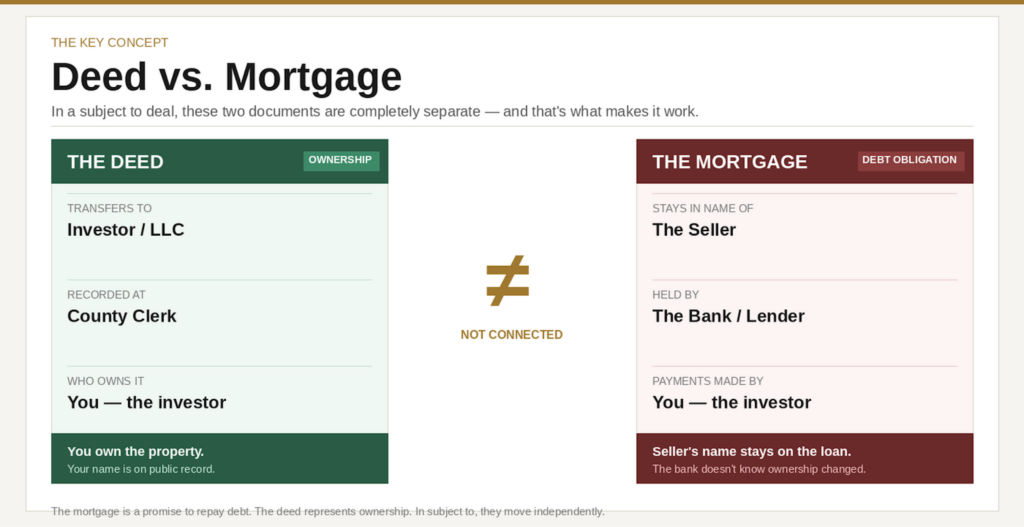

Subject 2 real estate is a creative financing strategy which means acquiring a property without taking out a new mortgage. The deed transfers into your name or your entity, whether that’s an LLC or a land trust. The existing loan stays in place under the seller’s name. That’s Subject 2 mortgage explained in its simplest form.

You take responsibility for the mortgage payments, for the property’s condition, the taxes, the insurance, and the maintenance. To understand exactly what goes into those payments, including how principal, interest, taxes, and insurance work together, read my guide for the first-time home buyer. It breaks down the Principal Interest Taxes and Insurance (PITI) components every homeowner (and Subject 2 investor) needs to understand. This is what buying a house Subject 2 the existing mortgage actually looks like in practice.

Roger admitted this concept tripped him up when he first started.

"When I was new in this business, that was one of my biggest stumbling blocks. I just did not understand that the mortgage and the deed were not married or connected together. It took me a while to figure that out."

That separation matters. The mortgage is a promise to repay a debt. The deed represents ownership. When you buy Subject 2, you step into the owner’s shoes without stepping into their loan obligation.

Closing costs on a Subject 2 deal, assuming the seller is current on payments and you aren’t paying them for equity, typically run below $2,500. That’s significantly less than the down payment required on a conventional loan, which often runs 3% to 20% of the purchase price.

Typical Subject 2 Closing Costs:

- Title fees

- Title insurance

- Recording fees

- Both sides of the closing costs

The Biggest Misunderstanding: Deed vs Mortgage

Beginners get stuck here constantly. They assume that if the loan stays in the seller’s name, the seller still owns the house. That’s incorrect.

The seller transfers ownership to you at closing. They sign the deed over. You record that deed with the county. The public record shows you as the owner. The bank’s loan remains in the seller’s name, but you’re the one making payments.

This separation is why Subject 2 works. You can’t get a new loan at 3 percent today, but you can acquire a property that already has one. The bank doesn’t need to approve the ownership change because the loan continues performing.

Subject 2 Real Estate Risks

Let me be direct. Subject 2 real estate risks are real. Anyone who tells you otherwise hasn’t done enough deals or hasn’t been honest about their experience.

Here are the key risks every investor must understand:

- Due-on-sale clause – Banks retain the right to call the loan due if ownership transfers without their consent

- Refinance uncertainty – You cannot guarantee when or if refinancing will be possible

- Insurance mistakes – Mishandling insurance transitions can cost thousands

- Seller occupancy – Never let the seller stay after closing

- Expense responsibility – You’re on the hook for taxes, maintenance, and repairs

- Overpromising timelines – Promising seller removal by a specific date creates liability

Warning: The due-on-sale clause exists in nearly all conventional mortgages. While lenders rarely exercise it when payments continue arriving on time, the risk never disappears completely.

Roger addressed the refinance myth directly.

"A good investor will never say, 'I'll have your name off that loan in X amount of time.' There's no way to guarantee that. When I started my import-export business in 1980, I watched interest rates go from 7 percent to 18 percent in twelve months."

Insurance creates another hidden trap. Roger shared a story about an experienced investor with over one hundred Subject 2 properties who was paying double insurance on every house. He didn’t know how to properly handle the transition, and it cost him six figures annually.

Can You Remove the Seller From the Mortgage?

This question comes up constantly. Sellers want their names off the loan. The reality is more complicated. So, can you remove the seller from the mortgage Subject 2 deals? Not easily.

You cannot force a bank to release someone from a mortgage. The only ways to remove a seller are:

- Refinance into a new loan in your name

- Pay the mortgage off entirely

Refinancing depends on three factors outside your control:

- Market interest rates

- Your credit and income qualifications

- The property’s equity position

Roger works with investors who face this challenge regularly. One client acquired a block of properties from an older investor exiting the business. The original seller was promised removal within five years. But those properties carried loans at 3 percent. As of February 2026, refinancing today would mean rates in the high sixes according to Bankrate. The math doesn’t work.

"Never make a decision when somebody else is involved in that decision-making process. If an investor goes in and says, 'I'll have your name off this mortgage in five years,' they're making a promise they can't keep."

How Investors Find Subject 2 Deals

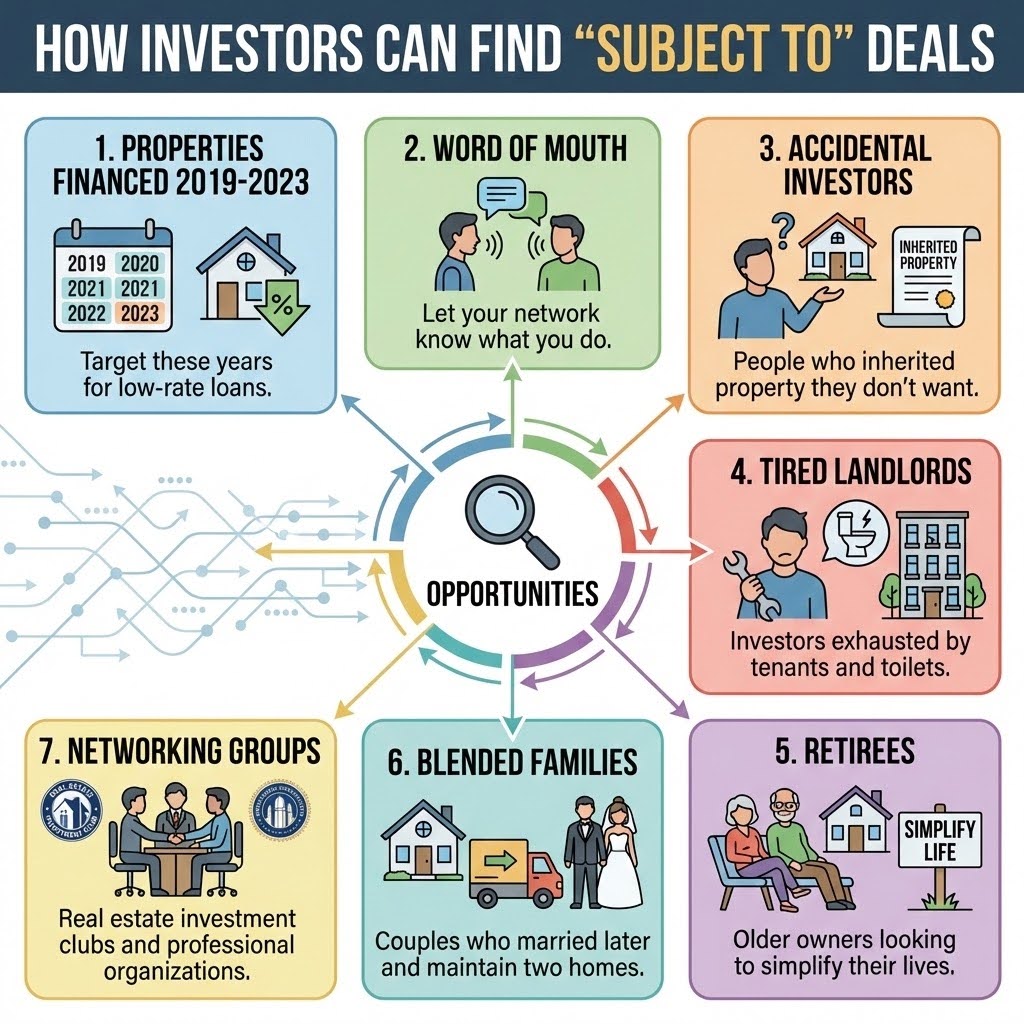

You find Subject 2 deals by looking for properties financed between 2019 and 2023. Those are the years when rates bottomed out. Software tools can filter for financing dates, helping you identify homes with assumable low-interest loans. This is how to find Subject 2 deals in today’s market.

Here are the most effective sources Roger uses:

- Properties financed 2019-2023 – Target these years for low-rate loans

- Word of mouth – Let your network know what you do

- Accidental investors – People who inherited property they don’t want

- Tired landlords – Investors exhausted by tenants and toilets

- Retirees – Older owners looking to simplify their lives

- Blended families – Couples who married later and maintain two homes

- Networking groups – Real estate investment clubs and professional organizations

One of Roger’s students, a twenty-year-old investor, picked up $1.8 million worth of real estate between December and January.

Success Story: A twenty-year-old investor acquired 11 houses worth $1.8 million from one individual who wanted out of the market — all in December before Christmas.

Sellers don’t know creative solutions exist. They know about listing with a realtor. They know about foreclosure. They don’t know about Subject 2. You have to approach them and offer a solution to their problem.

Subject 2 vs Owner Financing

These two strategies work together beautifully, but they serve different purposes. Understanding Subject 2 vs owner financing helps you use both effectively.

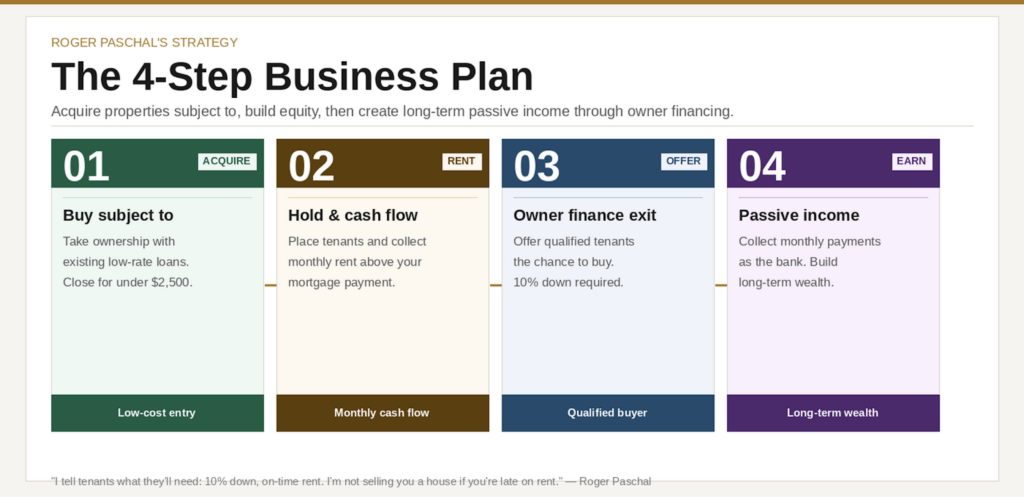

Roger’s preferred business plan follows a specific path:

- Acquire properties Subject 2

- Rent them for at least two years

- Offer owner financing to qualified tenants

- Create ongoing passive income

"I really work with that tenant saying, 'I would love to sell you this house one day.' I tell them what they'll need. Ten percent down payment. On-time rental payments. I'm not going to sell you a house if you're late on rent, because I know you'll be late on house payments."

Owner financing serves buyers who can’t access traditional mortgages:

- Business owners who don’t show enough income on tax returns

- People new to an area without established credit

- Individuals rebuilding credit after financial challenges

- Anyone needing an opportunity to build equity

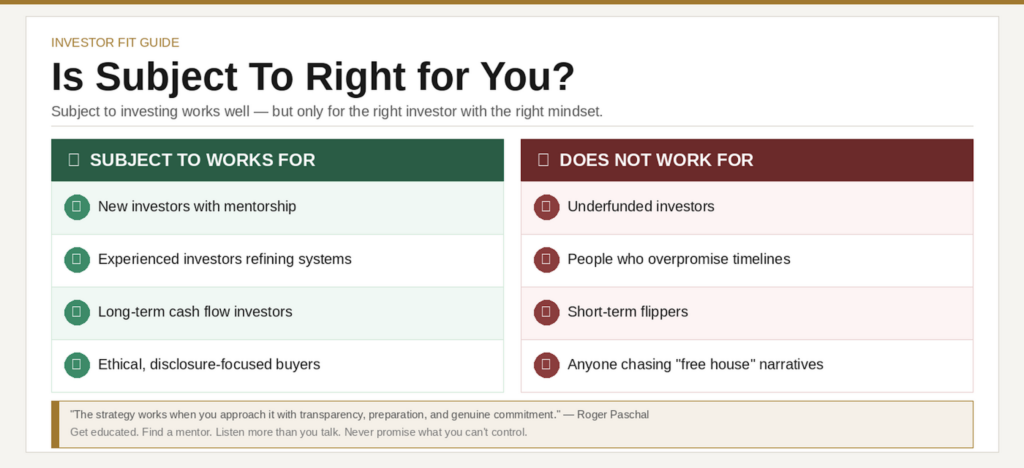

Who Should Use Subject 2 Real Estate

Subject 2 investing for beginners works when approached with humility and mentorship. But it’s not for everyone.

"People say that all the time. 'I got my house for free.' No, you didn't. There's a mortgage attached to it. But now you're going to put a tenant in there, and that tenant's going to pay that mortgage. They're going to pay the insurance and the taxes. They're going to pay down the principal. And you're getting cash flow above and beyond. I don't know any other investment where somebody else pays for everything, and you make money every month."

Owner financing serves buyers who can’t access traditional mortgages:

- Business owners who don’t show enough income on tax returns

- People new to an area without established credit

- Individuals rebuilding credit after financial challenges

- Anyone needing an opportunity to build equity

Frequently Asked Questions

-

Is Subject 2 real estate legal?

Yes, Subject 2 real estate transactions being legal in all fifty states. The key is proper disclosure and documentation. Work with a title company and real estate attorney who understands creative financing.

-

Can the bank call the loan due?

Banks retain the right to accelerate the loan under the due-on-sale clause as outlined in the Garn-St Germain Act (12 U.S.C. 1701j-3). This rarely happens when payments continue arriving on time, but the risk exists.

-

Is this a free house?

No. You assume responsibility for the mortgage, taxes, insurance, and maintenance. Closing costs typically run below $2,500.

-

What happens if the seller stops cooperating?

Proper documentation protects you. The deed transfers ownership at closing. You control the property.

-

What if interest rates drop?

Lower rates create refinancing opportunities. If rates drop significantly, you can refinance into a new loan in your own name. But never guarantee this timeline.

-

Is Subject 2 investing safe?

Safety depends entirely on your preparation. With proper education, ethical disclosures, and professional guidance, Subject 2 investing offers a legitimate path to building wealth. Without those elements, the risks multiply.

The Mindset That Makes Subject 2 Work

Subject 2 real estate offers a genuine opportunity in today’s high-rate market. But opportunity without education becomes a liability. Roger Paschal built his career on solving problems for homeowners while creating sustainable cash flow for himself and his students. That’s the model worth following.

The strategy works when you approach it with transparency, preparation, and genuine commitment to serving the people on the other side of the deal.

If you’re exploring creative financing for real estate or considering your first subject to deal with, take Roger’s advice. Get educated. Find a mentor. Listen more than you talk. And never promise what you can’t control.

For more investor success stories, visit Icons of Real Estate. The creative deal structuring framework shared in this conversation represents just one example of the real estate investor education available through our podcast network.

No Legal or Financial Advice DisclaimerThis material is provided solely for informational and educational purposes and does not constitute legal, tax, financial, real estate, or professional advice. Nothing contained herein should be relied upon as a substitute for consultation with licensed legal, tax, accounting, or financial professionals. The author, presenter, and associated entities expressly disclaim any liability for decisions or actions taken based on this content. Always seek qualified professional counsel regarding your specific circumstances. |

Listen Here

Apply as a Guest on The Falls Home Front

Real estate is evolving. Capital is shifting. Markets are tightening.

If you’re actively working in the industry and solving real problems, whether in construction, finance, brokerage, or development, we’d love to hear from you. The Falls Home Front showcases investors, agents, and industry professionals who are doing the work and creating real solutions for homeowners and communities.

This podcast is produced by the Icons of Real Estate – #1 Real Estate Podcast Network.

Interested in sharing your expertise? Apply to be a guest speaker on our network. For more resources, visit hub.iconsofrealestate.com.

About Tim Lockhart

Tim Lockhart, REALTOR®, is a RamseyTrusted real estate agent and retired U.S. Air Force Major serving Wichita Falls, Iowa Park, and Burkburnett, TX. Since becoming licensed in 2012, Tim has closed over 300 transactions, specializing in military relocation, listings, farm & ranch, and investment properties. He leads the Lockhart Real Estate Team at Keller Williams Realty and ranks among the top 10% of Keller Williams Lonestar DFW agents. Tim holds the MRP designation and has 45+ 5-star reviews across Zillow, FastExpert, and Google.- Is the Wichita Falls, TX Housing Market Going to Crash in 2026? - March 26, 2026

- Wichita Falls Housing Market Update – February 2026: Prices Are Up, But Here’s What That Really Means - March 23, 2026

- Where to Hunt Easter Eggs in Wichita Falls in 2026 - March 12, 2026

- Lake Wellington Estates | Growth & Development - March 6, 2026

- Jim Bousquet & Red River Dart Leagues Texas - March 4, 2026

- Homes for Sale in Wichita Falls TX | Prices & Guide - February 25, 2026

- Subject 2 Real Estate: Strategy, Risks & Execution - February 18, 2026

- Photo Booth Rental Wichita Falls, TX for Meaningful Events - February 11, 2026

- What Are the Steps to Buying Your First House in the Wichita Falls TX Real Estate Market? - February 5, 2026

- Wichita Falls Real Estate: Build Wealth and Find Your Dream Home - February 4, 2026