Wichita Falls Market Outlook

Every week, someone asks me the same question. They’ve seen the YouTube videos, the doom-scrolling headlines, the social media predictions comparing everything to 2008. So I decided to break it all down on The Falls Home Front Podcast using actual numbers: the 2026 Keller Williams Vision data, national economic indicators, and what I’m seeing on the ground as a realtor in Wichita Falls, Texas. The short answer to whether the housing market will crash in 2026 is no, and the data isn’t even close. The long answer requires understanding what a crash actually demands, where we stand nationally, and why Wichita Falls has its own fundamentals that most national pundits completely ignore.

I’m Tim Lockhart, and I serve the Wichita Falls community and Sheppard Air Force Base families. What I’ve found after digging through this year’s numbers is that the gap between how the market feels and how it actually performs has never been wider.

I pulled a few of the sharpest moments from this episode. Give them a watch below.

If you want the full picture, from what actually caused the 2008 crash to why Wichita Falls sits in a completely different position today, the entire conversation is here.

Market conditions shift fast, and I share the numbers as I see them. Follow along on Instagram for local field updates and LinkedIn for deeper market analysis.

Disclaimer: This video is for educational purposes only and reflects current market data at the time of recording. Real estate markets are influenced by many variables including employment trends, interest rates, and local supply and demand. For personalized financial, tax, or legal advice, consult a licensed professional.

Introduction: Why Everyone Is Asking About a Housing Market Crash

Fear about a potential crash is driving conversations everywhere right now, from social media feeds to gym parking lots. Mortgage rates sitting between 6 and 7% have made monthly payments feel drastically different from three years ago, and constant media comparisons to the 2008 crisis have people genuinely on edge. The noise is loud, and most of it is wrong.

Headlines aren’t data. To understand whether the Wichita Falls TX housing market forecast for 2026 points toward a crash or something far less dramatic, I looked at the indicators that actually move home prices:

- Mortgage rates and their historical context

- Housing inventory at both national and local levels

- Unemployment trends and their direct impact on foreclosures

- Buyer demand and what’s driving or stalling it

What follows is the full breakdown, national trends first, then what those numbers mean specifically for Wichita Falls.

What Would Actually Cause a Housing Market Crash?

The word “crash” gets thrown around loosely, so let’s pin it down. A real housing market crash means prices falling 20 to 30% and foreclosures spiking to crisis levels. That’s exactly what happened in 2008, and it was driven by a specific set of conditions:

- Loose lending standards that put people into homes they couldn’t afford

- Subprime mortgages structured to fail

- Massive overbuilding in markets like Phoenix, Las Vegas, and Florida

- Unemployment spiking above 9%

- Speculative investing with minimal skin in the game

Today, almost none of those conditions exist. Lending standards are significantly tighter than they were in 2006. Distressed sales make up only about 2% of total transactions nationally. Nearly 40% of homes are owned free and clear, and the household debt-to-income ratios across the country confirm that homeowners sit in a far stronger equity position than they did before 2008.

If you want to track how these national trends play out locally, my Wichita Falls market reports break down the numbers for this area specifically.

Key National Indicators for the 2026 Housing Market Housing Inventory

Inventory is measured in “months of supply,” the number of months it would take to sell every active listing assuming no new listings and steady buyer activity each month. A balanced market sits at roughly six months. Nationally, we’re still well below historical oversupply levels, even after recent inventory increases. Wichita Falls never had the overbuilding that hit Phoenix, Las Vegas, or Florida in 2006, and these are fundamentally different markets with different dynamics.

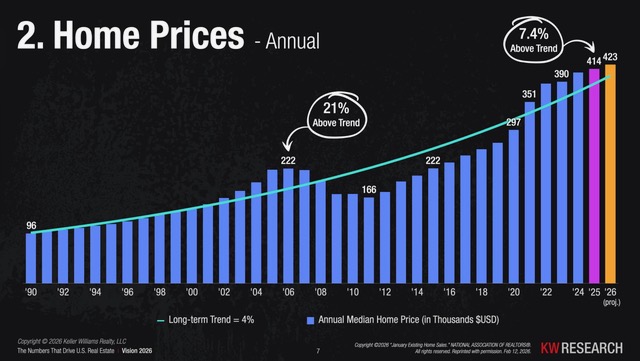

According to the 2026 Keller Williams Vision data, home prices nationally sit about 7.04% above the long-term trend line. That’s worth watching, but it’s nowhere near the 25 to 40% premiums that defined the pre-2008 bubble. Historically, prices rarely decline outside of major recession-level unemployment events, and the Vision data clearly shows that home prices only drop when unemployment spikes above 9%.

Market Comparison Table

Market Indicator | 2008 Crash Period | 2026 Market Outlook |

Lending Standards | Loose | Strict |

Inventory Levels | Oversupply | Limited |

Foreclosures | High | Historically Low (~2%) |

Homeowner Equity | Low | Record High |

Unemployment | Spiked above 9% | Stable near 4% |

Speculative Activity | Widespread | Minimal |

Total dollar volume tells the same story. The 2026 Vision data projects this to be the third highest volume market ever recorded outside of the COVID spike years. Fewer transactions are happening, but higher prices sustain overall volume. That’s normalization, not collapse.

Mortgage Rates and Historical Perspective

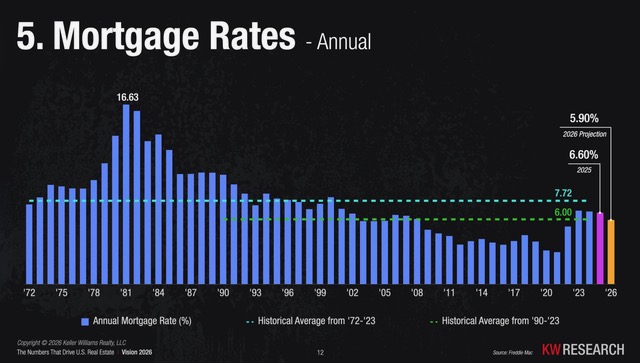

Rates hovering around 6 to 7% feel steep because buyers are measuring them against the 2020 to 2021 window when rates briefly dipped below 3%. The long-term average since the 1970s is approximately 7.7%. Today’s rates are elevated compared to three years ago, but they’re historically normal, and that’s the perspective most headlines leave out entirely.

Americans currently spend about 32% of their income on principal and interest. In the 1980s, when rates hit 18%, affordability levels were dramatically worse than anything we’re seeing today. Compared to long-term history, we aren’t in crisis territory.

Homeowner Equity and Locked-In Mortgages

Over 50% of homeowners nationally hold mortgage rates under 4%, and nearly 40% carry no mortgage at all. That creates a lock-in effect with real consequences for inventory:

- Fewer sellers: Trading a 3% rate for a 7% rate makes no financial sense for most homeowners, so they’re choosing to stay put.

- Minimal distressed sales: High equity means owners can sell traditionally if needed, avoiding foreclosure entirely.

- Low foreclosure risk: The equity cushion that didn’t exist in 2008 protects today’s homeowners from forced selling.

The data doesn’t support a mass sell-off scenario. Most owners are in a position of strength, and they’re staying rather than selling into a rate environment that works against them. That lock-in effect is the single biggest reason inventory remains tight heading into 2026.

Wichita Falls TX Housing Market Forecast for 2026

National headlines miss local dynamics entirely, and Wichita Falls runs on a completely different set of fundamentals than Austin, Phoenix, or Miami. Our market is anchored by three pillars: military demand from Sheppard Air Force Base, healthcare employment from the regional medical center, and a stable manufacturing base. We don’t see wild price spikes, and that means we don’t see violent corrections either. Appreciation here tends to be steady, boring, and healthy. That’s actually a strength.

I’ve worked with military families relocating to and from Wichita Falls for years, and the consistency of PCS-driven demand creates a floor under this market that speculative Sun Belt cities simply don’t have. Military demand creates stability. Speculation creates crashes. The upcoming 2026 Military and Veterans Resource Fair is one more example of the kind of community investment that keeps Wichita Falls grounded.

Why Wichita Falls Tends to Remain Stable:

- Consistent military housing demand tied to Sheppard Air Force Base

- Moderate, steady population growth without boom-and-bust cycles

- Limited new construction that prevents oversupply

- Diversified employment across military, healthcare, and manufacturing sectors

Current Housing Inventory in Wichita Falls

Wichita Falls currently sits at approximately four months of inventory, below the six-month benchmark for a balanced market. That means we have a healthy real estate market, leaning slightly toward sellers without the chaos that defined 2020 and 2021.

Inventory Type Table

- 0 to 3 months: Seller’s market, where low supply drives heavy competition and price increases

- 4 to 6 months: Balanced market (Wichita Falls sits here at 4 months, with room for healthy activity)

- 7+ months: Buyer’s market, signaling the kind of oversupply that can push prices down

Four months of inventory supports price stability. We’re nowhere near the oversupply threshold that precedes meaningful declines.

Will the Wichita Falls Housing Market Crash?

For a crash to hit Wichita Falls, we’d need unemployment spiking dramatically, large-scale foreclosure waves, massive oversupply of new construction, or widespread investor sell-offs. None of that is happening. Unemployment sits near 4% and holding steady. Distressed sales hover around 2% of transactions. Homeowner equity is at record levels. And this market never had the speculative overbuilding that hammered Sun Belt cities before 2008.

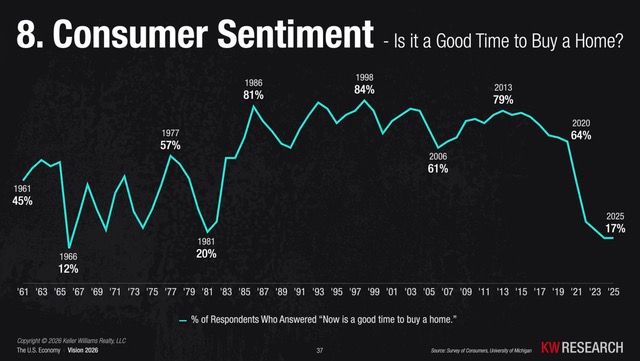

Consumer sentiment tells an interesting story. Only about 17% of Americans say it’s a good time to buy, but that metric has been low before: during the 18% rates of 1981, the Vietnam escalation in the mid-1960s, and inflation spikes in the 1970s. Each time, real estate still appreciated over the following decades. People tend to evaluate housing through a 10-year memory window, but real estate moves in 30 and 50-year cycles. Feelings don’t equal fundamentals.

The consistent theme from real estate practitioners I talk to across the country is the same: the conditions required for a crash aren’t present. Anyone asking will the housing market crash in 2026 should look at these fundamentals before making decisions based on headlines.

What Buyers and Sellers Should Expect in 2026

The realistic scenario for 2026 is market normalization: slower appreciation, increased negotiation leverage, and heightened price sensitivity from buyers. That’s healthy, and it’s an environment where strategy matters more than hype.

Buyer Opportunities:

- More inventory options than the past three years

- Increased negotiation flexibility on repairs and closing costs

- Fewer bidding wars and less frantic competition

First-time homebuyers currently sit at about 21% participation, compared to a historical norm closer to 40%. That gap signals hesitation and uncertainty, not a credit bubble, and it’s very different from forced selling. Reduced competition creates real advantages for buyers ready to act. My home buying resources walk through what the process looks like in today’s Wichita Falls market.

Seller Strategies:

- Price accurately. The days of throwing a number at the wall and waiting to see what the market brings are finished. This is a strategy market now.

- Prepare the home. Buyers have more choices and will pass on properties that aren’t move-in ready.

Why Real Estate Rewards Time in the Market

Historical housing appreciation averages around 4% annually. Look at where Wichita Falls home prices sat 15 years ago and you’ll see values have roughly doubled. That’s what consistent long-term growth does, quietly and without headlines, compounding year after year.

“Real estate doesn’t reward timing the market; it rewards time in the market.”

The 2026 Vision data reinforces this. If you bought at the absolute peak of 2006, when prices were 21% above the trend line and right before the worst crash in modern history, you’d still be significantly ahead today. That’s what long-term appreciation does. Waiting for a crash that median home price trends don’t support means missing years of equity growth that you never get back. Every decade, people say they wish they’d bought sooner. We’re in one of those moments right now.

If you’re a military family PCS-ing to Wichita Falls or a long-term investor weighing your options, reach out. I’d love to have that conversation, because perspective beats panic every single time.

Frequently Asked Questions

Will the housing market crash in 2026?

Most economic indicators don’t support a housing market crash in 2026. Inventory remains limited, foreclosure rates sit at historic lows, and homeowner equity is at record highs. The more likely outcome is slower appreciation and gradual market normalization rather than a price collapse.

Will the Wichita Falls housing market crash?

The Wichita Falls market remains stable due to consistent military demand from Sheppard Air Force Base and diversified employment across healthcare and manufacturing. Current inventory at four months indicates a balanced market, not the oversupply that triggers crashes.

Will home prices drop in Wichita Falls, Texas?

Prices may experience slower growth or brief stabilization periods, but significant declines are unlikely without major economic disruptions such as mass unemployment or a dramatic spike in new construction supply.

Is 2026 a good time to buy a home in Wichita Falls?

2026 presents better buying conditions than recent years, with more inventory and increased room for negotiation. Historically, buyers who focus on time in the market rather than timing the market build more wealth over the long run.

This podcast is produced by the Icons of Real Estate – #1 Real Estate Podcast Network

Listen Here

Apply to Be a Guest on The Falls Home Front Podcast

Questions like will the housing market crash in 2026 deserve answers grounded in local data, not national panic. If you’re an agent, investor, or industry expert bringing that kind of clarity to your market, we want to hear from you.

About Tim Lockhart

Tim Lockhart, REALTOR®, is a RamseyTrusted real estate agent and retired U.S. Air Force Major serving Wichita Falls, Iowa Park, and Burkburnett, TX. Since becoming licensed in 2012, Tim has closed over 300 transactions, specializing in military relocation, listings, farm & ranch, and investment properties. He leads the Lockhart Real Estate Team at Keller Williams Realty and ranks among the top 10% of Keller Williams Lonestar DFW agents. Tim holds the MRP designation and has 45+ 5-star reviews across Zillow, FastExpert, and Google.- Is the Wichita Falls, TX Housing Market Going to Crash in 2026? - March 26, 2026

- Wichita Falls Housing Market Update – February 2026: Prices Are Up, But Here’s What That Really Means - March 23, 2026

- Where to Hunt Easter Eggs in Wichita Falls in 2026 - March 12, 2026

- Lake Wellington Estates | Growth & Development - March 6, 2026

- Jim Bousquet & Red River Dart Leagues Texas - March 4, 2026

- Homes for Sale in Wichita Falls TX | Prices & Guide - February 25, 2026

- Subject 2 Real Estate: Strategy, Risks & Execution - February 18, 2026

- Photo Booth Rental Wichita Falls, TX for Meaningful Events - February 11, 2026

- What Are the Steps to Buying Your First House in the Wichita Falls TX Real Estate Market? - February 5, 2026

- Wichita Falls Real Estate: Build Wealth and Find Your Dream Home - February 4, 2026